Open Banking

with Noda

Features and Integrations

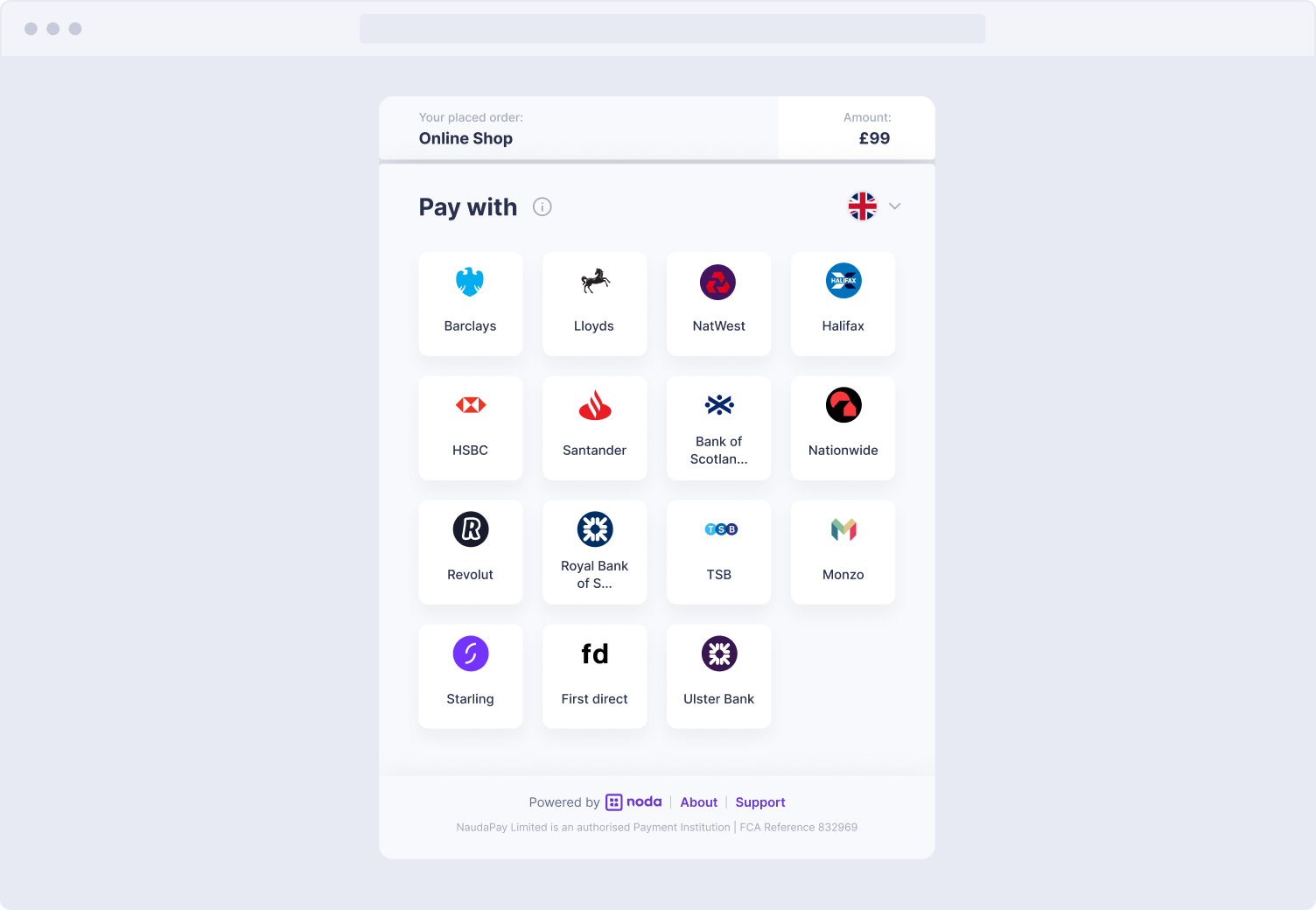

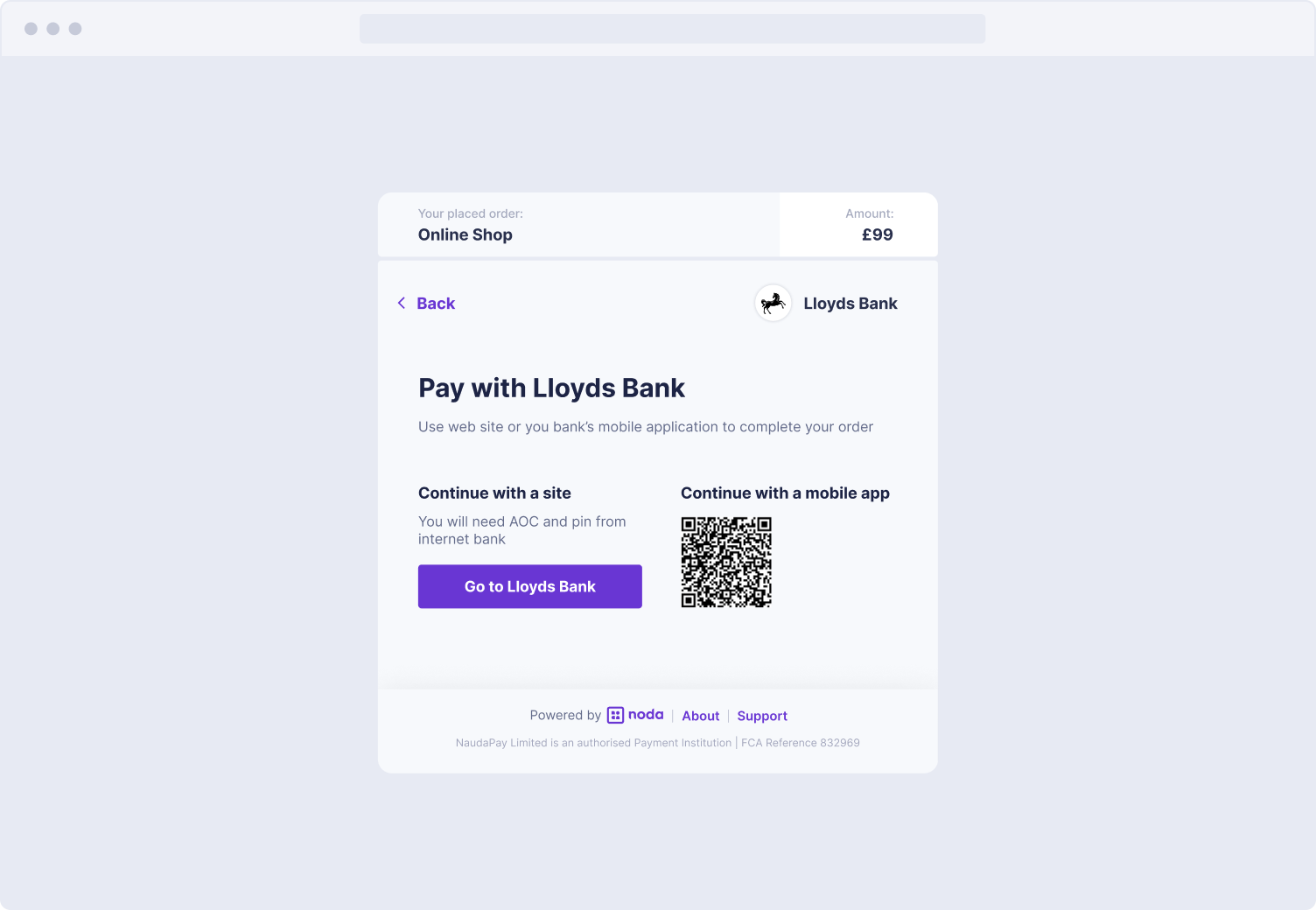

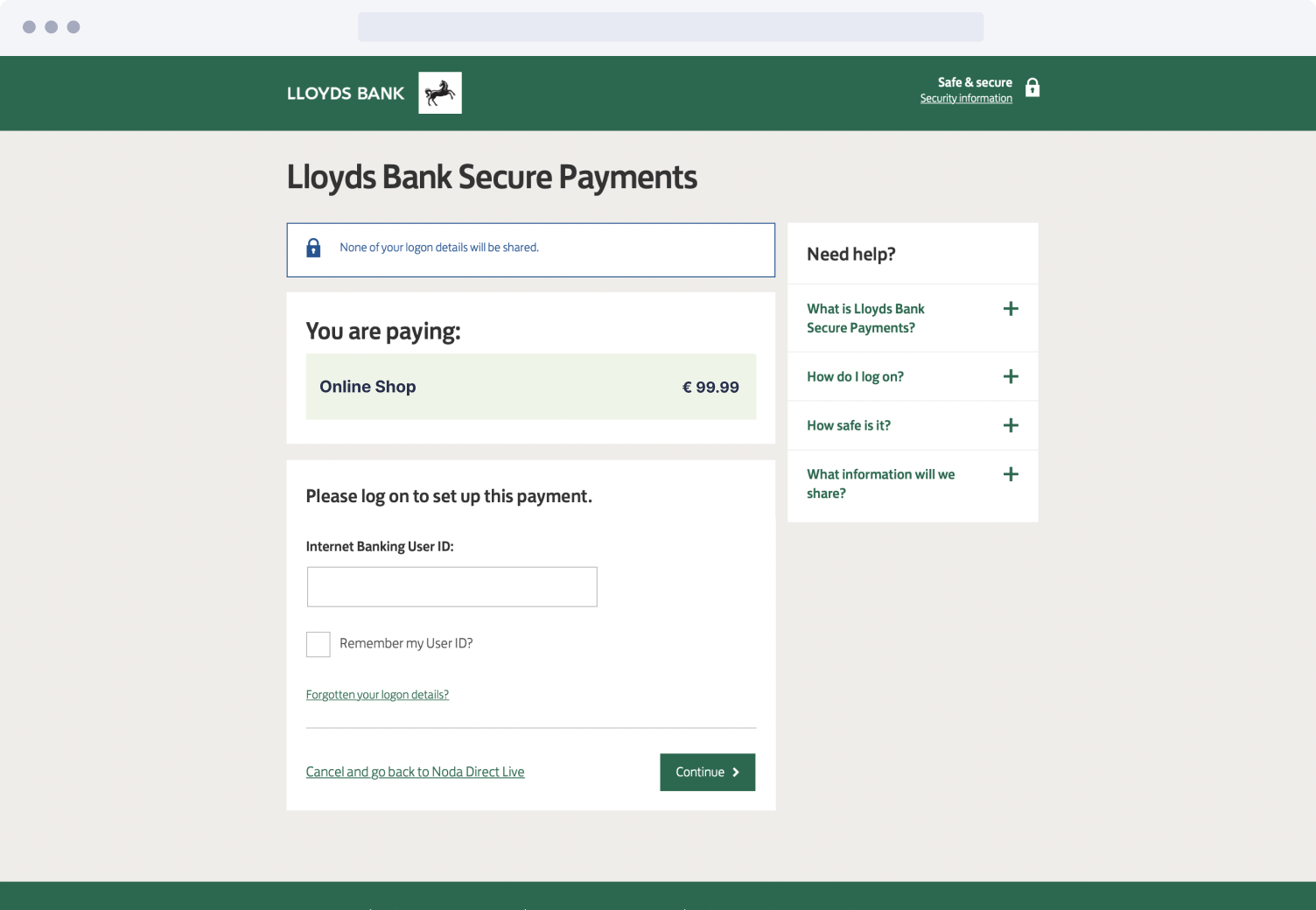

How Our Open Banking Solution Works

from features to integrations

2000+ banks

Learn about Noda coverage

Key Features

Secure Transactions

Smooth Integration

Personal Manager

Analytics

Refunds

Trusted Banks

Multiple Roles

C2B Accounts

Blacklists

FIRST STEPS

Easy Onboarding

With a Personal Manager

Special Features

Trusted Payments

to Accelerate your Checkout

Tech Friendly

Seamless Integration for Better Payments: Launch in Hours, Not Weeks

curl --request POST \--url https://api.noda.live/api/payments \--header 'Accept: application/json, text/json, text/plain' \--header 'Content-Type: application/*+json' \--header 'x-api-key: 01e7d75e-0cc2-42ea-a463-f16348e34cdd' \--data '{"amount": 1.24,"currency": "EUR" ,"customerId": "CID-012456789-1" ,"description": "Order 1234-DS-1234" ,"shopId": "d0c3ccd9-162c-497e-808b-e769aea89c58" ,"paymentId": "119318-123-test-1423" ,"returnUrl": "https://myshop.com/returnurl" ,"webhookUrl": "https://myshop.com/hookurl" ,}'

Above 90%

Noda  —

—

Manage Everything You Need in One Place

Refunds

Multi Roles

Transactions

Reporting

Refunds

Multi Roles

Transactions

Reporting

Discover More Features

€316,884

Banking Experience

C2B Account

Management

Best conditions for every business

Scalable Plans to Meet Your Business Needs

Open Banking Payments

Card Payments

Checkout Form

Card Payouts

Bank Payouts

Data Enrichment

Virtual IBANs